The Reserve Bank is not a place given to big shows of emotion. When I worked there, it was full of incredibly hard-working and talented people, all of whom actively wanted to be there. The staff were very measured, and the tone of briefing papers was generally one of pacific calm. That’s difficult to do when you’re sitting on billions of dollars in the basement, while simultaneously guarding the nation’s financial system stability. To the people who work there – I doff my cap.

The most razzmatazz the Bank generally gets is when the Governor and the Monetary Policy Committee launch a Monetary Policy Statement (MPS). Analysts pour over every word, seeking to divine secrets of the future like latter-day soothsayers. The colour of the words used by the Bank are inspected by Journalists to see if there is a change in the thinking of the Bank about interest rates (and with it, the national obsession – house prices). In the Beehive, Political Advisors cross whatever they have and pray for a good news story on the TV at 6pm.

Today was one of those days of excitement, the February MPS. As ever, the real juice is not in the documents or the speeches, but in the attached Excel spreadsheets. Specifically, the tab marked ‘projections’. That tells you what the Bank really thinks about the future, stripped of all the soothing words placed elsewhere. If you study them, they also give you an insight into how the Bank’s thinking has evolved over-time.

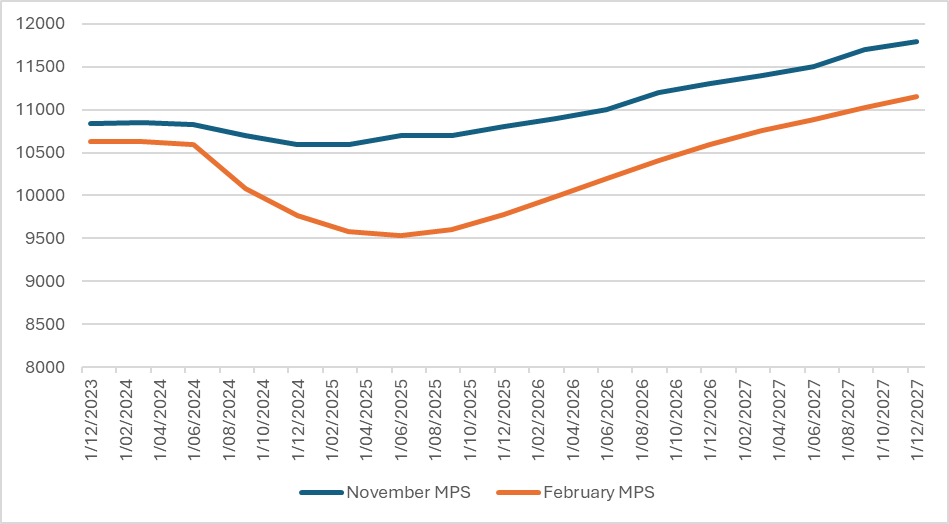

Take employment. The Reserve Bank forecasts that employment levels won’t reach the employment levels found at the election until March 2026. Essentially we will have had two and a bit years of zero employment growth. We haven’t seen that sort of stagnation in 15 years. This set of forecasts is 60,000 cumulative jobs worse off than the forecast in November.

Figure 1: Employment in New Zealand (000’s) – Recorded and Forecast

Source: RBNZ Data

The Reserve Bank uses a ‘heat map’ of labour market pressures to show how well it performing on a range of measures. Broadly speaking, the redder the chart is, the tighter the labour market. Again, the chart shows a rapidly cooling labour market, with the tighter labour market of the past now being firmly behind us.

Figure 2: Labour Market Indicators - Reserve Bank Map

Source: RBNZ, Feb MPS

Partly this weaker labour market is driven by lower business investment. The government has been very clear that it sees businesses investing in New Zealand as the key to making sure the economy grows. Sadly, the levels of business investment found at the election don’t return until early-2027 in real terms. Across the forecast period business investment is cumulatively forecast to be $8.3bn lower in real terms than at the forecast in November 2024. That’s really going to hurt the government’s ambition to ‘go for growth’.

Figure 3: Forecast Real Business Investment ($m)

Source: RBNZ Data

House prices are also not turning up. New Zealand’s economic model for a long time has been:

Rising house prices = Wealth Effect = Spending = Jobs = Rising house prices (Repeat)

(Except if you are young, poor, Māori, Pasifika, on a benefit, disabled, or live in an unfashionable town. Sorry, your brand of growth is currently unavailable)

To some extent more modest increases in house prices are quite desirable over the forecast period (till the end of 2027). House prices are due to increase by 11%, instead of the 16% in the November forecasts. It suggests a soggy economy – not doing much – hoping for something to turn up.

The bank data shows that sogginess extends to the residential investment – which again is lower than the forecast in November. It is cumulatively $4.4bn lower across the next three years. That means fewer houses being built, and fewer people in construction. A sector that has already seen nearly 13,000 fewer people working in than this time last year. Residential investment doesn’t return to levels seen at the election until September 2026 (in real terms).

Figure 4: Quarterly Forecast Residential Investment ($m’s)

Source: RBNZ Data

So this soggy growth should feed through to soggier inflation right? Fewer people being employed, businesses investing less, fewer houses being built – it’s a recipe for falling inflation aye? Er…the honest answer is no. Inflation actually picks up in the short-run. It is forecast to rise to 2.7% in September this year – dangerously flirting with the edge of the 1% - 3% target band.

The driver for this short-run increase is oil pricing – which is being driven by a lower NZ dollar (as oil prices are priced in US dollars, we need more of them to buy the same amount of oil). Cuts to interest rates weaken the NZ Dollar further – meaning that oil prices rise higher in NZ Dollar terms. Oil prices tend to drive higher prices everywhere in New Zealand. It’s almost as if it makes economic sense not to be reliant on oil.

There are also a range of risks that mean we should take a return to higher inflation seriously. If Donald Trump succeeds in getting new tariffs installed then it is very likely to mean higher US inflation – tariffs are paid by consumers not producers. That will entail higher US interest rates (pushing the NZ Dollar lower). Counter-tariffs around the world will make all trade globally more expensive. As a trading nation – New Zealand gets both higher inflation and lower GDP. Ace.

So what does all this mean?

Last Saturday I wrote about the government not appearing to have a plan for the economy – and that the ‘going for growth’ report appeared to be little more than a slogan. This data shows why this is important. On these projections New Zealand is continuing to drift.

These projections are generally speaking worse than those produced by the Reserve Bank last year. Recent evidence from the US suggests that consumers there are expecting inflation to remain at 3% - at the top of their target range. That means fewer interest rate cuts and a higher US Dollar. The NZ business price index fell in the last quarter as energy prices fell (in particular wholesale electricity pricing). That helped overall CPI but it’s not a trick that will be repeated as electricity future pricing is showing much higher prices for later this year.

Above all the data tells us that there are likely to be two future scenarios for the economy and potentially our politics. From someone who cares about building a stronger, more equitable economy in Aotearoa – neither of them look good.

SCENARIO 1 – Back to the Future

In this scenario, we essentially go back to the economy we had in the recent past. We rely heavily on a few sectors such as dairy and tourism. Unemployment is higher than it needs to be. Interest rates stay low, as we try and build an economy based on selling houses to each other and “Hello” by Adele is playing on the radio all the time like it’s 2015. We don’t invest in creating a more diverse economy, or having any actual infrastructure except for roads and that which we can bundle together as PPP opportunities. We pretend that claims about having a ‘rockstar’ economy mean something.

In this scenario, the government would claim that it has won the economic argument at the next election. It would have done extremely little to justify that claim, but it will be made based on the fact that things are marginally better than they were a few months prior. Anyone looking at the child poverty numbers might disagree, but the housing shows on TV will make us think that things are finally heading back into place.

SCENARIO 2 – Back to Back Inflation

In this scenario, we find out what the lack of a resilient economy really means. Inflation continues to rise, as tariffs and global growth grind trade down. Unemployment doesn’t stop at 5.2% as the current forecasts predict. We end up cutting spending to balance the books, at the same time as demand in the economy falls. Even the soggy growth predicted in the MPS today fails to event, and our trading partners – particularly China – see weak growth.

In this scenario the government blames:

a) The previous government

b) The global economy

c) Woke banks

d) Free school meals

e) Road cones

None of these will be true. We will have engineered a classic demand-deficient recession. Opportunities to fix this situation with domestic fiscal stimulus will be sacrificed on the altar of getting the OBEGALx/OBEGALy/OBEHAVE (delete as appropriate by 2026) back into surplus. The government will claim that only it can deliver the changes that will solve our problems - despite being the same solutions that actually got us into this mess.

In both scenarios, we are rediscovering what the great economist Keynes meant when he said that monetary policy is like ‘pushing on a string”. Increasing interest rates can be very effective in helping to rein in inflation – i.e. pulling on the string. But they aren’t very good when the opposite problem occurs – getting growth going again sustainably.

That relies on having healthy workers with skills who can take up new opportunities. It relies on having new sectors of growth so that you don’t simply push against the growth constraints you already had. It means investing in infrastructure so that firms and entrepreneurs can take advantage of opportunities. It means not immiserating the population to the point they leave.

Actual fiscal responsibility. The stuff the government is choosing not to do. We can choose better.

Thank you Craig, your wisdom and sense of humour are appreciated.

And a new priority for spending public money is being introduced - increased defence spending i.e. transferring $ to the US military-industrial complex. More important than reducing child poverty or improving pour public health system or taking effective pre-emptive measures against climate breakdown and natural disasters.